As you can see, by extending the loan term, the payments become substantially lower (even if the interest rate is above 0%). This often has an impact on what car you can afford.

If you take the 0% financing, the dealer will not offer you the same discount off the price of the car. Remember, lenders don’t give money away for free. The manufacturer and/or dealer is paying the lender to give you the benefit of 0% financing. That money has to come from somewhere so it is usually built into the price of the car.

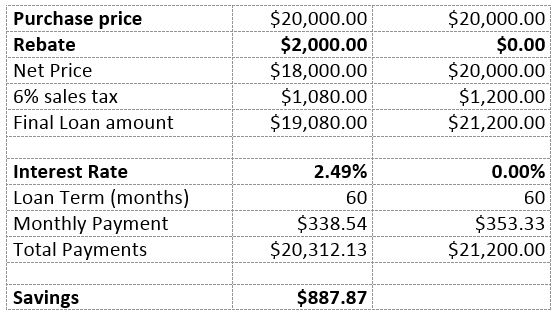

Opting for the rebate instead of the 0% financing will reduce the overall price of the car. This means in the future, when you are ready to trade in the car you will not owe as much (assuming you still have a loan balance). The amount you receive for your trade-in may even be enough to pay off your existing loan balance.

In some states, the rebate reduces the purchase price of the car which in turn results in a reduction in the sales tax. If the rebate is $2,000 and there is a 6% sales tax the rebate will save you $120 in sales tax. Pro Tip: If your state does not allow this ask the dealer to reduce the price by the amount of the rebate and not list the rebate on the sales order in order to reduce your sales tax.

For our discussion let’s assume the purchase price of your new vehicle is $20,000 (dream on) and the manufacturer is offering a $2,000 rebate or 0% financing for 5 years. We will assume no additional discounts and that your credit score is in the 700-750 range. We will ignore the cost of title and tags as these are the same in both instances.